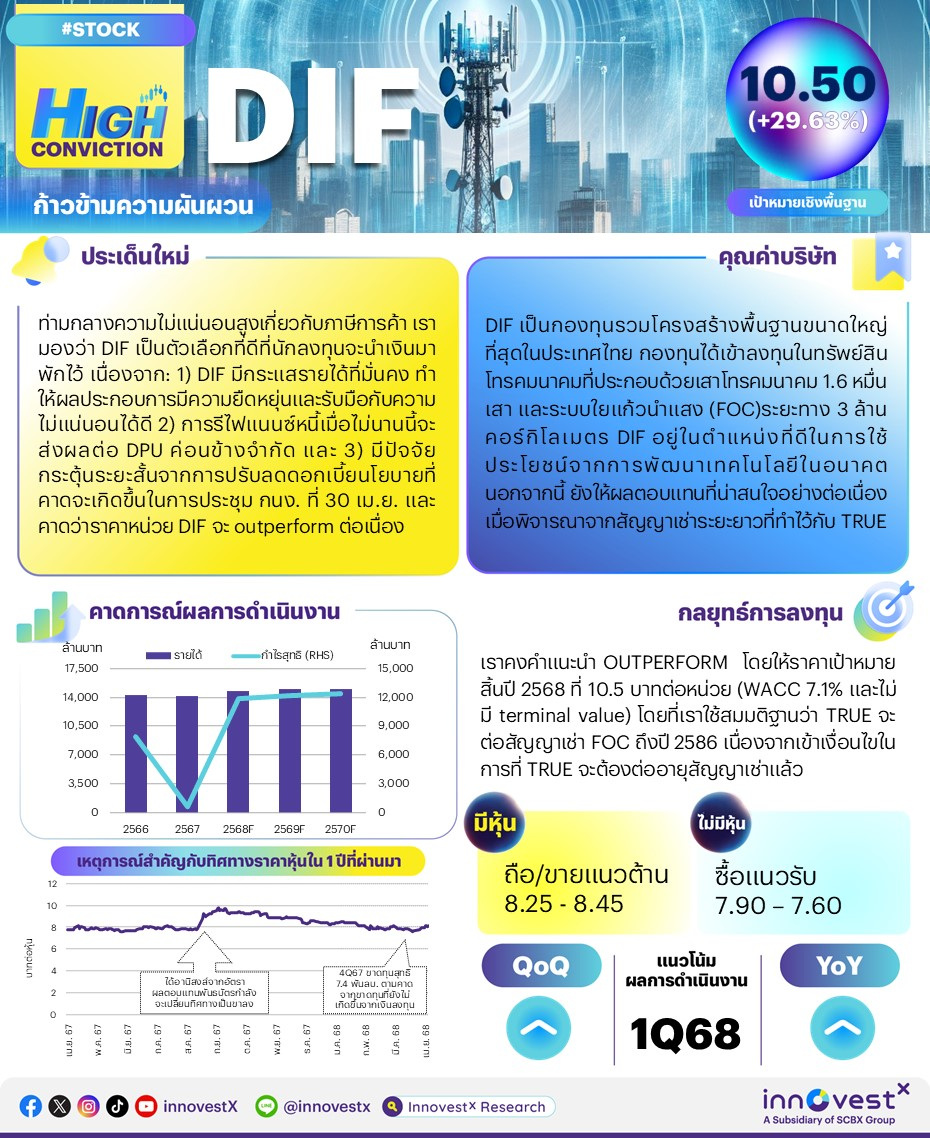

ท่ามกลางความไม่แน่นอนสูงเกี่ยวกับภาษีการค้า เรามองว่า DIF เป็นตัวเลือกที่ดีที่นักลงทุนจะนำเงินมาพักไว้ เนื่องจาก: 1) DIF มีกระแสรายได้ที่มั่นคง ทำให้ผลประกอบการมีความยืดหยุ่นและรับมือกับความไม่แน่นอนได้ดี 2) การรีไฟแนนซ์หนี้เมื่อไม่นานนี้จะส่งผลกระทบต่อ DPU ค่อนข้างจำกัด และ 3) มีปัจจัยกระตุ้นระยะสั้นจากการปรับลดอัตราดอกเบี้ยนโยบายที่คาดว่าจะเกิดขึ้นในการประชุม กนง. วันที่ 30 เม.ย. ราคาหน่วยลงทุน DIF ปรับตัว outperform SET ตั้งแต่ต้นปี 2568 ถึงปัจจุบัน และคาดว่าจะ outperform ต่อเนื่อง เราคงคำแนะนำ OUTPERFORM สำหรับ DIF โดยให้ราคาเป้าหมายสิ้นปี 2568 อ้างอิงวิธี DCF ที่ 10.5 บาท/หน่วย (WACC 7.1% และไม่มี terminal value) โดยที่เราใช้สมมติฐานว่า TRUE จะต่อสัญญาเช่า FOC ถึงปี 2586 เนื่องจากเข้าเงื่อนไขในการที่ TRUE จะต้องต่ออายุสัญญาเช่าแล้ว

ปัจจัยกระตุ้น #1: ผลประกอบการมีความยืดหยุ่นในการรับมือกับความไม่แน่นอนที่สูง ตลาดยังคงเผชิญกับความไม่แน่นอนสูงจากผลกระทบของภาษีทรัมป์ ทำให้ DIF เป็นตัวเลือกลงทุนที่น่าสนใจ เนื่องจากมีกระแสรายได้ที่มั่นคง ใน 1Q68 เราคาดว่า DIF จะรายงานกำไรปกติที่ 3 พันลบ. เพิ่มขึ้น 1.7% YoY และ 0.8% QoQ รายได้ค่าเช่าคาดว่าจะอยู่ที่ 3.5 พันลบ. เพิ่มขึ้น 0.4% ทั้ง YoY และ QoQ เราคาดว่ารายการต้นทุนหลักๆ จะอยู่ในระดับทรงตัว YoY และ QoQ ยกเว้นดอกเบี้ยจ่าย ซึ่งเราคาดว่าจะลดลง 4.2% YoY และ 1.6% QoQ มาอยู่ที่ 520 ลบ. ซึ่งเป็นผลมาจากอัตราดอกเบี้ยที่แท้จริงที่ลดลง เนื่องจากเงินกู้ของกองทุนมีอัตราดอกเบี้ยลอยตัว กำไร 1Q68 ที่เราประเมินได้คิดเป็น 25% ของประมาณการกำไรเต็มปีของเรา เราคาดว่า DIF จะประกาศจ่าย DPU งวด 1Q68 ที่ 0.22 บาท/หน่วย โดยกองทุนจะประกาศผลประกอบการในวันที่ 14 พ.ค.

ปัจจัยกระตุ้น #2: การรีไฟแนนซ์หนี้จะส่งผลกระทบต่อ DPU เพียงเล็กน้อย DIF ต้องรีไฟแนนซ์หนี้จำนวน 1.2 หมื่นลบ. ในเดือนมี.ค. 2568 จากหนี้คงค้างรวม 2.48 หมื่นลบ. เราคาดการณ์ไว้ก่อนหน้านี้ว่าการรีไฟแนนซ์หนี้ดังกล่าวจะทำให้ DPU ปรับลดลงมาอยู่ที่ 0.81 บาท/หน่วย ในปี 2568 ข้อมูลล่าสุดที่เราได้มาจากทาง DIF พบว่าการรีไฟแนนซ์หนี้ครั้งนี้ รวมการชำระคืนเงินต้นจำนวน 1.3 พันลบ. ในปี 2568 ด้วย หรือสูงกว่าปี 2567 อยู่ 100 ลบ. ทำให้ปัจจุบันเราคาดว่า DPU ในปี 2568 จะอยู่ที่ 0.88 บาท/หน่วย ซึ่งแม้ว่าจะต่ำกว่า DPU ปี 2567 ที่ 0.89 บาท/หน่วย อยู่เล็กน้อย แต่เรายังมองว่ายังอยู่ในเกณฑ์ที่ดี

ปัจจัยกระตุ้น #3: การปรับลดอัตราดอกเบี้ยนโยบายที่คาดว่าจะเกิดขึ้นในการประชุม กนง. วันที่ 30 เม.ย.INVX คาดว่า กนง.จะปรับลดอัตราดอกเบี้ยนโยบายลงอีก 25bps ซึ่งจะส่งผลดีต่อ DIF ในสองทาง ทางแรก คือ การปรับลดอัตราดอกเบี้ยนโยบายจะทำให้อัตราผลตอบแทนจากเงินปันผลของ DIF ดูน่าสนใจมากขึ้นเมื่อเทียบกับพันธบัตรรัฐบาล ทางที่สอง คือ เนื่องจากหนี้ของ DIF มีอัตราดอกเบี้ยลอยตัวและเชื่อมโยงกับอัตราดอกเบี้ยนโยบาย การปรับลดอัตราดอกเบี้ยลงทุกๆ 25bps จะหนุนให้กำไรสุทธิของ DIF ปรับเพิ่มขึ้นได้ปีละ 70 ลบ. ทั้งนี้ INVX คาดว่าจะมีการปรับลดอัตราดอกเบี้ยนโยบายลงอีก 2 ครั้ง (ครั้งละ 25bps) ในปีนี้ คือ ในการประชุมเดือนมิ.ย. และครึ่งหลังของปี 2568

กลยุทธ์การลงทุนและคำแนะนำ ราคาหน่วยลงทุน DIF ปรับตัว outperform SET อยู่ 11.4% ตั้งแต่ต้นปี 2568 ถึงปัจจุบัน และเราคาดว่าจะ outperform ต่อเนื่อง DIF ให้ผลตอบแทน 2.7% สำหรับระยะเวลาถือครอง 1 เดือน นอกจากนี้เรายังเล็งเห็นปัจจัยกระตุ้นระยะสั้นจากการปรับลดอัตราดอกเบี้ยนโยบายในวันที่ 30 เม.ย. ด้วย ความเสี่ยง downside ต่อกำไรของ DIF ยังคงมีจำกัดเมื่อพิจารณาจากกระแสรายได้ที่มั่นคง

ปัจจัยเสี่ยงและความกังวล อัตราผลตอบแทนพันธบัตรที่สูงขึ้นจะทำให้เงินปันผลดูน่าสนใจน้อยลง และจะทำให้ราคาหน่วยลงทุนมี upside จำกัด เนื่องจาก DIF จัดอยู่ในกลุ่มหุ้นปันผล

Amid high uncertainty over the tariffs, we see DIF as a good place for investors to park funds as: 1) DIF has a stable income stream, making its earnings resilient, 2) there is limited impact on DPU from its recent debt refinancing and 3) it has a near term catalyst from the expected policy rate cut at the April 30 MPC meeting. The share price outperformance of the SET YTD is expected to continue. We maintain OUTPERFORM with an end-2025F DCF-based TP of Bt10.5 (7.1% WACC and no terminal value). We assume TRUE will renew the FOC lease through 2043, as conditions have been met.

Catalyst#1: Resilient earnings amid high uncertainty. The market is still facing high uncertainty over the impact of Trump’s tariffs. This puts DIF in the spotlight as an entity with a stable revenue stream. In 1Q25F, we expect DIF to report core profit of Bt3bn, up 1.7% YoY and 0.8% QoQ. Rental income is expected to be Bt3.5bn, growing 0.4% both YoY and QoQ. We expect the main cost items to be stable YoY and QoQ, except for interest expense, which we estimate will fall 4.2% YoY and 1.6% QoQ to Bt520mn on a lower effective interest rate since its loans are floating-rate. Our 1Q25F estimates work out to 25% of our full-year forecast. We expect the fund to announce a 1Q25F DPU of Bt0.22. Results will be released on May 14.

Catalyst#2: Small impact on DPU from debt refinancing. DIF has to refinance Bt12bn debt in Mar 2025 from total outstanding debt of Bt24.8bn. We had expected this would lower its DPU to Bt0.81 in 2025F. Our most recent update from DIF shows that the debt financing includes principal repayment of Bt1.3bn in 2025 or Bt100mn higher than in 2024. On this basis, we now expect a 2025F DPU of Bt0.88. Although this is slightly lower than the 2024 DPU of Bt0.89, we see it as still decent.

Catalyst#3: Potential policy rate cut at the April 30 MPC meeting. INVX expects the MPC to cut policy rate another 25bps. This would help DIF in two ways. Firstly, it will make its yield more attractive against government bonds. Secondly, since DIF’s debt is floating-rate and linked to policy rate, each 25bps cut in interest rate adds Bt70mn p.a. to DIF’s bottom line. Note that INVX expects two more rate cuts this year, at the June and 2H25 meetings (25bps each).

Action & recommendation. DIF share price has outperformed the SET by 11.4% YTD and we expect the outperformance to continue. DIF offers 2.7% yield for a one month holding period. We also see a near-term catalyst from the policy rate cut on April 30. Downside to its earnings is also limited given its steady income stream.

Risk and concerns. The rising bond yield makes dividend less attractive and thereby caps upside to share price as DIF is considered a yield play.

Download PDF Click > DIF_HighConviction250428_E.pdf

Download PDF Click >