PDF Available

สรุปประเด็นการลงทุน

- ราคาน้ำมัน: ราคาน้ำมันดิบเบรนท์เฉลี่ยใน 1Q68 อยู่ที่ US$75.71 สอดคล้องกับประมาณการปี 2568 ของ INVX ที่ US$75/บาร์เรล แต่ปัจจุบันเราเชื่อว่าปัจจัยที่ส่งผลกระทบต่อราคาน้ำมัน โดยเฉพาะมาตรการเก็บภาษีนำเข้าทั่วโลกของสหรัฐฯ มีแนวโน้มที่จะทำให้ราคาน้ำมันปรับตัวลดลงในช่วงที่เหลือของปีนี้ โดยราคาน้ำมันยังมีความเสี่ยงขาลง

- ค่าการกลั่นน่าผิดหวังใน 1Q68 โดย -36% QoQ สู่ระดับต่ำสุดในรอบ 4 ปีที่ US$3.2/บาร์เรล แต่คาดว่าจะฟื้นตัวใน 2Q68 โดยจะเพิ่มขึ้นเล็กน้อย QoQ เนื่องจากอุปสงค์น้ำมันเบนซินจะเพิ่มขึ้นหลังจากอ่อนแอใน 1Q68

- แรงกดดันต่อค่าการตลาดน้ำมันจะลดน้อยลง แต่การแข่งขันรุนแรงมากขึ้น ธุรกิจการตลาดน้ำมันค้าปลีกจะยังคงเผชิญกับความท้าทายจากอุปสงค์ที่ชะลอตัวลงจาก GDP ที่เติบโตในระดับต่ำ

- แนวโน้มธุรกิจปิโตรเคมีจะได้รับผลกระทบจากนโยบายคุ้มครองการค้าของสหรัฐฯ แม้ว่าจีนจะมีมาตรการกระตุ้นการบริโภคภายในประเทศก็ตาม

- ผลประกอบการ 1Q68 ไม่มีทิศทางที่ชัดเจน โดยผู้ประกอบการโรงกลั่นน้ำมันจะได้รับผลกระทบจากค่าการกลั่นที่อ่อนแอ ขณะที่บริษัทค้าปลีกน้ำมันจะได้รับประโยชน์จากแรงกดดันที่ลดน้อยลงต่อค่าการตลาด

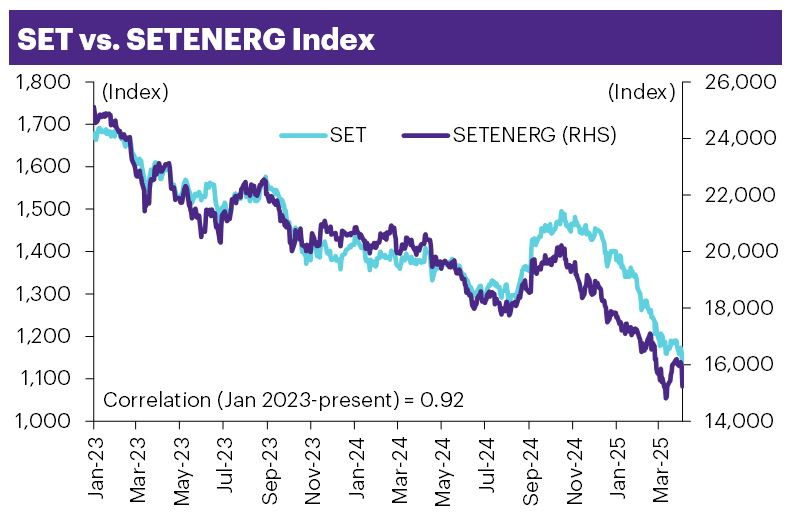

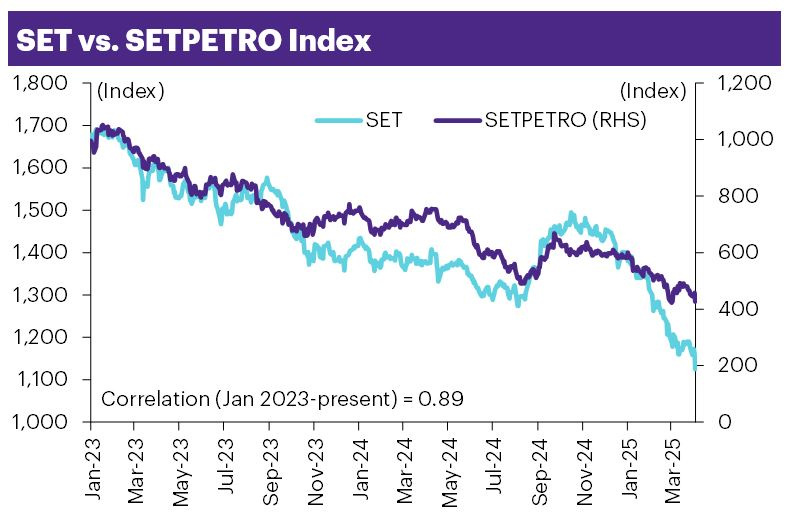

- เราให้น้ำหนักการลงทุน Neutral ต่อกลุ่มพลังงาน (น้ำมันและก๊าซ) และกลุ่มปิโตรเคมี โดยเลือกหุ้นรายตัวที่มีโมเดลธุรกิจแบบครบวงจร: BCP (ราคาเป้าหมาย 47 บาท) และ PTT (ราคาเป้าหมาย 41 บาท) นอกจากนี้เรายังชอบ PTTGC เพราะผลประกอบการมีแนวโน้มปรับตัวดีขึ้นจากปริมาณวัตถุดิบอีเทนที่สูงขึ้น และ valuation ถูก

- ปัจจัยเสี่ยง: (1) ภาวะเศรษฐกิจชะลอตัว (เป็นลบต่ออุปสงค์พลังงานและผลิตภัณฑ์ปิโตรเคมี) (2) ความผันผวนของราคาน้ำมัน (ขาดทุนสต๊อก) ความเสี่ยงอื่นๆ ได้แก่ การด้อยค่าของสินทรัพย์และการเปลี่ยนแปลงกฎระเบียบเกี่ยวกับการปล่อยก๊าซเรือนกระจก และการแทรกแซงของรัฐบาลในธุรกิจพลังงาน ปัจจัยเสี่ยงด้าน ESG ที่สำคัญ คือ ผลกระทบทางสิ่งแวดล้อม

Investment summary

- Oil price: Average Brent crude was US$75.71 in 1Q25, in line with the INVX forecast for 2025 of US$75/bbl, but we now believe the factors affecting oil price – especially the US global tariffs - are likely to dampen it for the remainder of the year. Oil price is still skewed to the downside.

- GRM disappoints in 1Q25, -36% QoQ to a 4-year low of US$3.2/bbl but expected to recover in 2Q25 with a slight increase QoQ as demand for gasoline will pick up after a weak 1Q25.

- Pressure on oil marketing margin to soften but competition is heating up. Retail oil marketing will continue to face challenges from the slowing demand caused by low GDP growth.

- Petrochemical outlook could be hurt by the US trade protectionism despite China stimulus to boost domestic consumption.

- Mixed 1Q25F earnings outlook with oil refineries to be hit by weak GRM. Oil retail could benefit by lower pressure on marketing margin.

- We are Neutral on energy (oil & gas) and petrochemicals with selective picks, choosing those with an integrated business model: BCP (Bt47) and PTT (Bt41). We also like PTTGC on improving earnings on higher ethane supply and cheap valuation.

- Risk factors: (1) an economic slowdown (negative for demand for energy and petrochemical products), (2) oil price volatility (stock losses). Other risks are asset impairment and regulatory changes on GHG emissions and government intervention in the energy business. Key ESG risk factors are the environmental impact.

Download EN version click >> ENEGY&PETRO(Presentation)250408_E.pdf

Author

ชัยพัชร ธนวัฒโน

Most Read

1

2

News update Thai StocksNews Update - การแพทย์ ความกังวลเรื่องประกันสุขภาพเอกชนจะมีการปรับกรมธรรม์เป็นแบบ Co-payment มากขึ้น => ยังต้องติดตามแต่มองว่าผลกระทบที่อาจจะเกิดขึ้นนั้นไม่มากNews Update - การแพทย์ ความกังวลเรื่องประกันสุขภาพเอกชนจะมีการปรับกรมธรรม์เป็นแบบ Co-payment มากขึ้น => ยังต้องติดตามแต่มองว่าผลกระทบที่อาจจะเกิดขึ้นนั้นไม่มาก

3

4

Related Articles

Most Read

1

2

News update Thai StocksNews Update - การแพทย์ ความกังวลเรื่องประกันสุขภาพเอกชนจะมีการปรับกรมธรรม์เป็นแบบ Co-payment มากขึ้น => ยังต้องติดตามแต่มองว่าผลกระทบที่อาจจะเกิดขึ้นนั้นไม่มากNews Update - การแพทย์ ความกังวลเรื่องประกันสุขภาพเอกชนจะมีการปรับกรมธรรม์เป็นแบบ Co-payment มากขึ้น => ยังต้องติดตามแต่มองว่าผลกระทบที่อาจจะเกิดขึ้นนั้นไม่มาก

3

4